In the first article of this series, I discussed the consumer lawsuit from the perspective of the consumer as defendant, meaning the consumer received a lawsuit from a creditor, debt collector, or debt buyer. In this article, Part II, I want to discuss when a consumer might consider suing a creditor, debt collector, or even credit reporting agency (Equifax, Experian, or Trans Union). I want to say what I said last article, very few people like lawsuits, they can be time consuming and emotionally draining. Consumers file suit against collectors at a far lower rate than collectors sue consumers. Unfortunately, there are times where a lawsuit may need to be filed by a consumer to stop abusive practices against them or to correct inaccurate information causing serious consequences. Here are two instances when a lawsuit may be the consumer’s only real option.

1. If after the consumer has tried all of the self-help strategies available and the collector or credit agency is refusing to comply with the law, a lawsuit may be necessary to protect the consumer’s legal rights. There are many, many steps a consumer can take to try and work with a collector or credit reporting agency, whether the debt is owed. Here are some resources for different types of consumer problems that outline what the consumer can do on their own, without legal assistance:

A. Identity Theft. If the consumer is a victim of identity theft there are steps to dispute debts and credit reporting items that do not belong to the victim. If the consumer follows these steps, and the collector or credit reporting agency refuses to comply with the law, a lawsuit may be necessary.

B. Collector Harassment. Even when a consumer owes the money, there are federal laws that protect consumers from misrepresentation and abuse by collectors. A great resource describing the limitations on debt collectors, what they are allowed to say or do, and not allowed to say or do is available on the Consumer Financial Protection Bureau Website. If the collector continues to violate the law, a lawsuit may be necessary.

C. Credit Reporting Errors. If the consumer has already disputed mistakes on their credit reports with Experian, Equifax, and TransUnion. The steps for consumers to order a free report from each of the bureaus and dispute any items on the report is found on this Federal Trade Commission Link. It is important to note that the credit reporting agencies are just that, reporting information provided by the “furnishers” of information- creditors, collectors, debt buyers, the IRS, bankruptcy courts, etc. If there is an issue with the organization that granted credit, the consumer must make sure to address the dispute with the furnisher as well.

2. If the Consumer is sued by a collector, creditor, or debt buyer, violations by these organizations may be grounds for a counter-suit (cross-complaint) at the time the consumer is sued. When the consumer has suffered frustrating months leading up to a lawsuit by a collector who does not follow the law, the consumer may bring a counter claim against the collector. In the last article, I talked about when a consumer receives a lawsuit, but if the consumer has been a victim of abuse, harassment, misrepresentation, etc, these claims can often be brought in court even when the consumer has been served.

A collector or creditor does not get a pass on following the law just because the consumer is sued to collect a debt. If a consumer receives a lawsuit, they should speak with an attorney. Look to local legal aid societies or find a “debt defense” or “consumer law” attorney for help. The consumer must respond to any lawsuit quickly, and if counter-claims are available, they must be filed with the answer. If the consumer is represented by an attorney, the collector can only talk to the attorney, and no longer contact the consumer directly.

State Laws for Consumers and Other Protections for the Military

It is also important to note that most states have consumer protection statutes, many that are similar to the federal statutes. For Example, In California there is a body of law under the Unfair and Deceptive Acts ad Practices (UDAP) that protect consumers. This means that the collector may have violated state law, and there may be a lawsuit in state court available to the consumer to protect their legal rights. If the consumer is a military member (or dependent in some cases) there are specific laws such as the Servicemen’s Civil Relief Act (SCRA) and the Military Lending Act (MLA) that may be available to a military consumer. The military consumer can contact the local Judge Advocate General’s (JAG) office for assistance.

The Consumer Must Preserve Their Rights by Keeping all Letters and Starting a Call Log. First, the consumer should save EVERY piece of correspondence received from a debt collector or creditor. If a law firm sends a letter trying to collect, save it. Start a folder and save everything. Second, start a call log. Texts, calls, and email messages. There are rules about identifying themselves as a collector, and a requirement to let the consumer know they are calling to collect a debt.

Note when a phone call is received or when the consumer makes one, who they talked to, any promises made, and what the outcome of the call was. In this day and age, we have caller ID, and we can note the date and time of calls, voicemail messages, and hang ups. It is critical that the consumer preserve this proof that they are receiving calls in violation of the law. And many collectors call in violation of the law. Either too early in the morning, or too late, or at work, or even after the consumer requests they stop calling.

Also note the outcome of the conversation. Did the collector promise to send something? Promise to remove the consumer form the auto-dialer? Promise not to call because the consumer made a promise to pay, “next Friday?” Write it down. And as frustrating as it may be, dealing with the collector, the consumer must not BREAK THE LAW themselves. The collector will advise the consumer that the call is being recorded, but depending on state law, the consumer may not record the conversation. Write it down.

Part III of this series on the Consumer Lawsuit will address what the consumer should expect (in most instances) if they decide to file a lawsuit against a creditor, collector or credit reporting agency. Unlike the collectors who often have teams of lawyers (or are lawyers), many consumers do not have an advocate, know where to get one, or are afraid of the costs involved. These are all real concerns, particularly if the consumer is already in financial trouble.

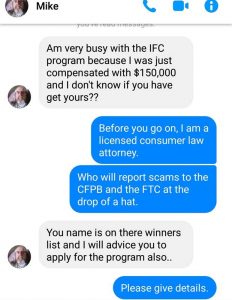

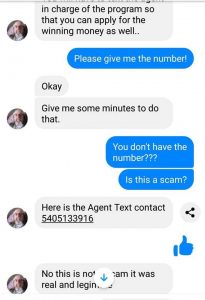

So, a Scammer DM’d a Consumer Law Attorney. Stop me if you’ve heard this one. It’s actually not funny at all, but it was for me, because I got the last laugh. Why? I immediately reported the attempted scammer to the Federal Trade Commission. I’m not alone, 1.4 Million people reported fraud to the FTC last year. Unfortunately, people also LOST $1.48 BILLION to fraud as well. People in their 20s made up of 43% of reporters, while people in their 70s made up only 15%. The median amount of loss to fraud last year was $400.00 for people in their 20s, and $751.00 for people in their 70s.

So, a Scammer DM’d a Consumer Law Attorney. Stop me if you’ve heard this one. It’s actually not funny at all, but it was for me, because I got the last laugh. Why? I immediately reported the attempted scammer to the Federal Trade Commission. I’m not alone, 1.4 Million people reported fraud to the FTC last year. Unfortunately, people also LOST $1.48 BILLION to fraud as well. People in their 20s made up of 43% of reporters, while people in their 70s made up only 15%. The median amount of loss to fraud last year was $400.00 for people in their 20s, and $751.00 for people in their 70s. 3. Fill out the form as completely as possible. If you receive a number, email, or even a social media conversation, please include that info. I took a screen shot of mine, so I had it to report.

3. Fill out the form as completely as possible. If you receive a number, email, or even a social media conversation, please include that info. I took a screen shot of mine, so I had it to report.

I hope everyone is having an amazing summer! Can you believe July 4th has passed us already? Since we are now into July, I suspect that back to school ads and sales are coming soon. I need to let you know about a proposed rule that the Consumer Financial Protection Bureau (CFPB) released regarding debt collection.

I hope everyone is having an amazing summer! Can you believe July 4th has passed us already? Since we are now into July, I suspect that back to school ads and sales are coming soon. I need to let you know about a proposed rule that the Consumer Financial Protection Bureau (CFPB) released regarding debt collection.

I had the amazing privilege to attend the Consumer Assembly last week in Washington DC, and there was a panel discussion on credit scoring. The panel was actually a discussion on a group of American consumers that are dubbed by the industry the, “Credit Invisibles.” These are people who cannot get a “good” credit score in the typical way, by having open lines of credit that are at least six months old. The industry that scores credit, including the Fair Isaac Corporation (FICO), the developers of the FICO credit scoring models, and Vantage Score Solutions, LLC, the developers of the Vantage credit scoring models, feel that “credit invisibles” are disadvantaged in receiving access to credit products. And they are, but this new model by FICO to address the credit invisibles and those with marginal credit is not good for consumers.

I had the amazing privilege to attend the Consumer Assembly last week in Washington DC, and there was a panel discussion on credit scoring. The panel was actually a discussion on a group of American consumers that are dubbed by the industry the, “Credit Invisibles.” These are people who cannot get a “good” credit score in the typical way, by having open lines of credit that are at least six months old. The industry that scores credit, including the Fair Isaac Corporation (FICO), the developers of the FICO credit scoring models, and Vantage Score Solutions, LLC, the developers of the Vantage credit scoring models, feel that “credit invisibles” are disadvantaged in receiving access to credit products. And they are, but this new model by FICO to address the credit invisibles and those with marginal credit is not good for consumers. “The hospital is saying that if we need a lower payment, we have to take out a loan.” I wouldn’t have believed it myself, but that statement came from my client. I actually was at a loss for words. “So, if you do not make the minimum payment the hospital has set you up with on the “plan” they won’t accept any payment at all?” Apparently, that is what the hospital told them. So, what to do if you are faced with this issue? Let’s talk about it.

“The hospital is saying that if we need a lower payment, we have to take out a loan.” I wouldn’t have believed it myself, but that statement came from my client. I actually was at a loss for words. “So, if you do not make the minimum payment the hospital has set you up with on the “plan” they won’t accept any payment at all?” Apparently, that is what the hospital told them. So, what to do if you are faced with this issue? Let’s talk about it.

Lots of news floating around about how a new legislative proposal where the federal government would take

Lots of news floating around about how a new legislative proposal where the federal government would take